Portuguese inheritance and gift law stands out in the European context for its tax competitiveness, particularly due to the absence of inheritance tax for direct family members and the application of reduced stamp duty rates. For foreign investors, international residents, and families with assets across multiple jurisdictions, understanding Portugal’s succession framework is essential for efficient and legally secure estate planning.

Succession

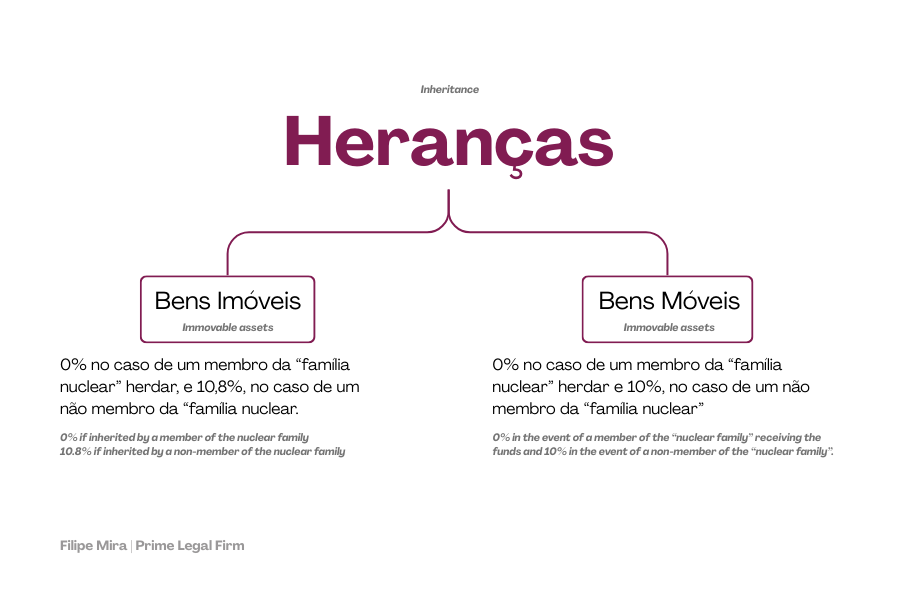

In Portugal, the “nuclear family”—which includes relatives in the direct line and spouses—pays 0% inheritance tax, a regime that is extremely favorable when compared with other European jurisdictions.

Even the “non-nuclear” family, which includes collateral relatives such as siblings, as well as third parties, benefits from an attractive tax regime. In these cases, heirs pay 10% on movable assets (cash) and 10.8% on real estate, which is still significantly lower than in many other European countries.

Given the current political landscape, we do not expect the introduction of a “hard” inheritance tax in the coming years.

Below, we attach a table summarizing the inheritance and donation tax regimes.*

For tax planning purposes, it may be advantageous to transfer movable assets (essentially cash) to Portugal. Provided that the country of origin does not impose an exit tax (i.e., a tax levied when assets are transferred to another jurisdiction), an individual may transfer funds to Portugal, where heirs will pay 0% tax upon succession.

The same applies to real estate located in Portugal, as heirs also pay 0% tax upon succession. Real estate located abroad raises more complex issues, as the country where the immovable property is situated may impose inheritance taxes.

Donations

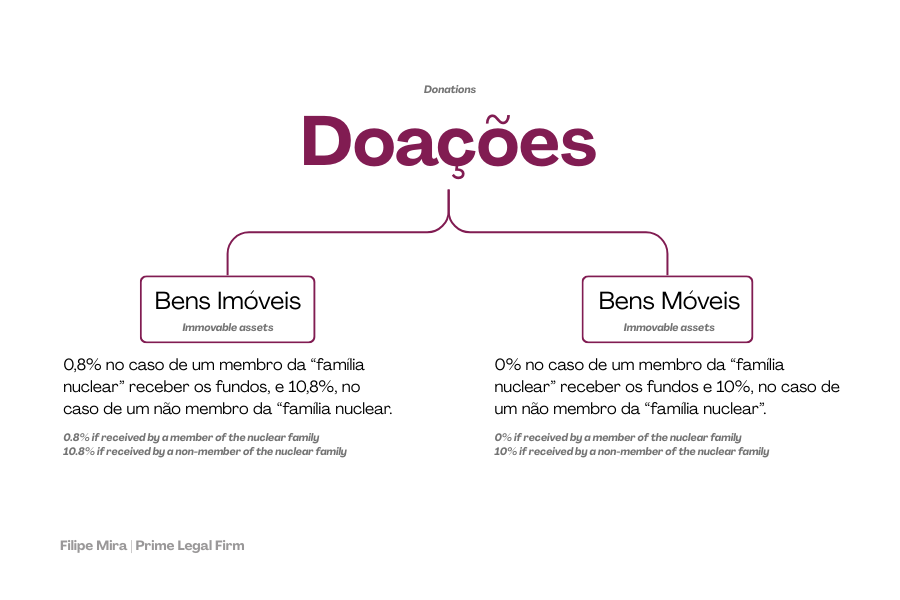

The legal framework governing donations is also favorable. Once again, the “nuclear family” benefits from significant protection, except in the case of donations of real estate, where a 0.8% tax applies. Donations of other assets are not taxed. For the “non-nuclear” family, a tax rate of 10.8% applies to real estate donations and 10% to movable assets (essentially cash).

From a tax planning perspective, Portugal is an excellent jurisdiction for transferring movable assets such as cash (subject to the considerations previously mentioned regarding immovable property located outside Portugal). I emphasize that colleagues in other jurisdictions should be consulted to ensure the most favorable overall tax treatment.

*Inheritance

*Donations

In summary, Portugal is a highly attractive jurisdiction for inheritances and donations, offering strong tax planning opportunities in both contexts. As previously noted, it is advisable to consult tax lawyers in other jurisdictions to achieve the most efficient overall tax outcome.

To avoid potential issues, it is strongly recommended that all interested parties reside in Portugal at the time of death or when a donation is made. A change of tax residence of both the deceased and the heirs to Portugal may be a decisive factor.

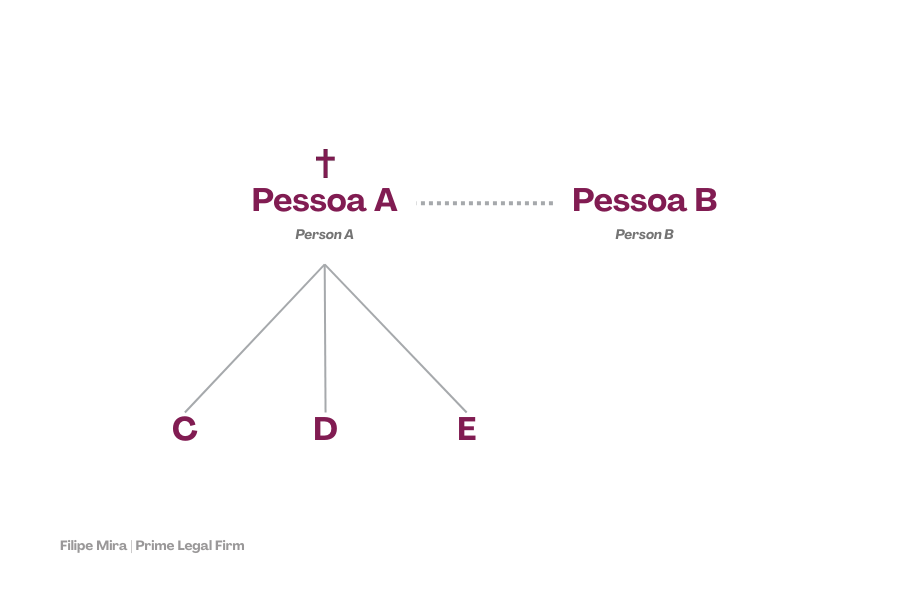

Under this framework, Person A dies. Person B, who is married to Person A, and their children (C, D, and E) pay 0% tax upon inheritance under Portuguese law. As previously mentioned, when part of the estate is located outside Portugal, consultation with foreign colleagues may be necessary.

This article does not replace consulting the relevant legislation, nor does it hold Prime Legal responsible.